It’s a game of opinions and Liverpool owners FSG – characterised either as Moneyball geniuses, self-interested hyper capitalists, or the best owners on the planet – inspire more than their fair share.

In reality, Fenway Sports Group are a bit of each. In October, it will be 15 years since the Boston-based owners bought Liverpool. In that time, it’s hard to argue they haven’t boxed above their weight class.

That Liverpool are routinely at the favourable end of the Premier League’s net spend table has become meme fodder in recent years, but to have done what they have on their recruitment budget is impressive.

Photo by Nick Taylor/Liverpool FC/Getty Images

Arne Slot has proved the perfect successor to Jurgen Klopp, equal parts continuity candidate and fresh ideas man. He will soon deliver the second league title of the FSG era.

| Position | Team | Played MP |

Won W |

Drawn D |

Lost L |

For GF |

Against GA |

Diff GD |

Points Pts |

| 1 | 29 | 21 | 7 | 1 | 69 | 27 | 42 | 70 | |

| 2 | 29 | 16 | 10 | 3 | 53 | 24 | 29 | 58 | |

| 3 | 29 | 16 | 6 | 7 | 49 | 35 | 14 | 54 | |

| 4 | 29 | 14 | 7 | 8 | 53 | 37 | 16 | 49 | |

| 5 | 29 | 14 | 6 | 9 | 55 | 40 | 15 | 48 | |

| 6 | 28 | 14 | 5 | 9 | 47 | 38 | 9 | 47 |

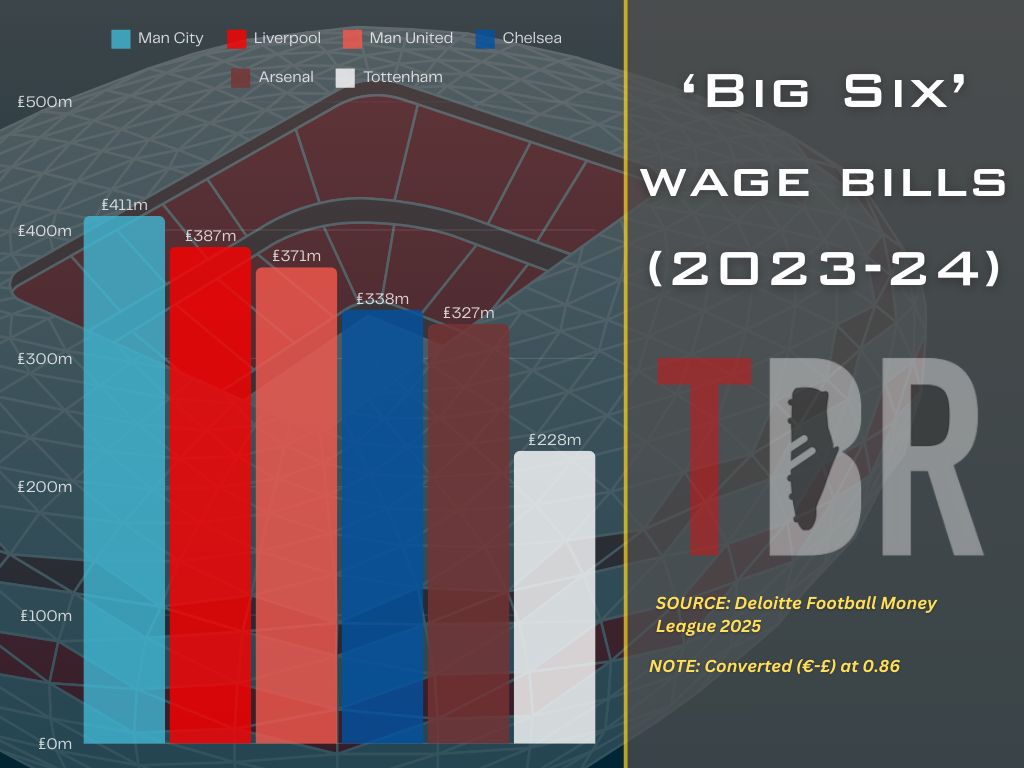

They will also finish the season with a positive net spend as far as headline transfer figures are concerned. Their wage bill, typically a far more accurate predictor of success, meanwhile is highly competitive.

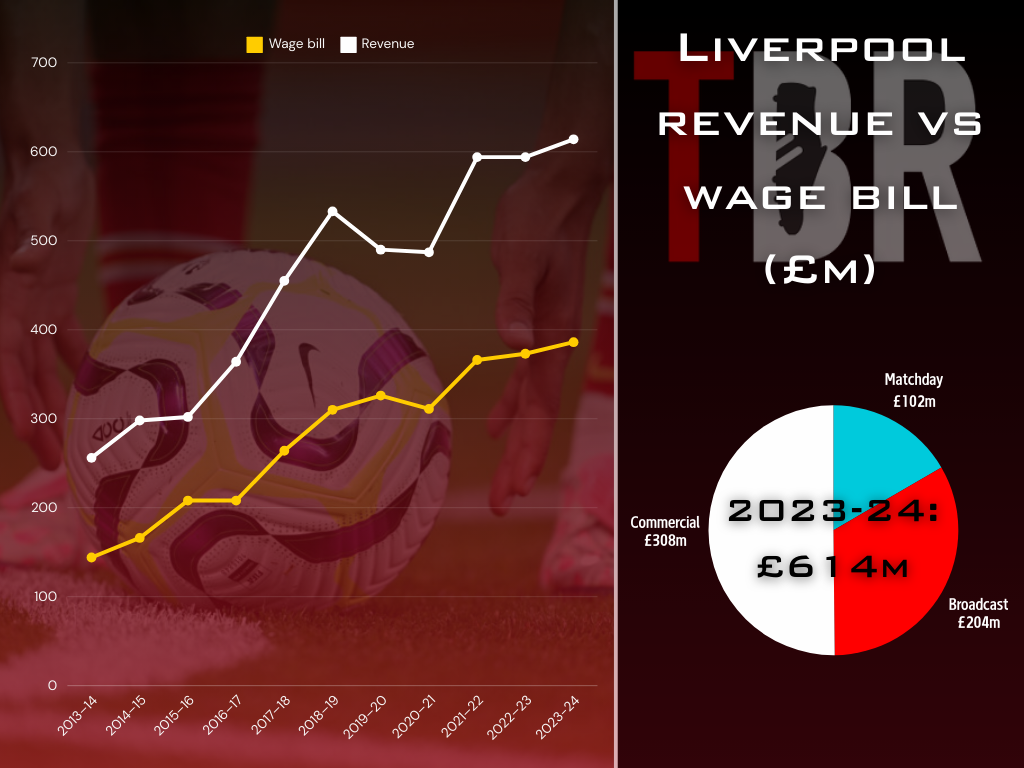

In 2023-24, a season when they didn’t even play in the Champions League with its associated bonuses, they paid out £387m, which was second only to Manchester City in the Premier League.

From next season, the payroll will shrink, with Trent Alexander-Arnold set to leave Liverpool for Real Madrid, despite FSG tabling what would have been a record contract offer.

It seems the 26-year-old had his heart set on the Bernabeu and there was ultimately little that the owners could do to stop him.

If Mohamed Salah and Virgil van Dijk leave, on the other hand, it will be a very different story.

This is the flipside to supporting an FSG-owned team. Decisions are made – or not made – based on what appears to be an overly cautious philosophy. Penny wise, pound foolish is the accusation from some fans.

On the other side of the Atlantic, supporters of the Boston Red Sox and Pittsburgh Penguins paint a similar picture.

The truth, however, is that every decision FSG make is backed up by terabytes of data and modelling based on various different contingencies. If John Henry and his deputies did it, they meant it.

Nearly every sports investor will tell you that it is an addictive pursuit and that winning trophies is the ultimate rush. But in their final analysis, the goal is to make money, not friends.

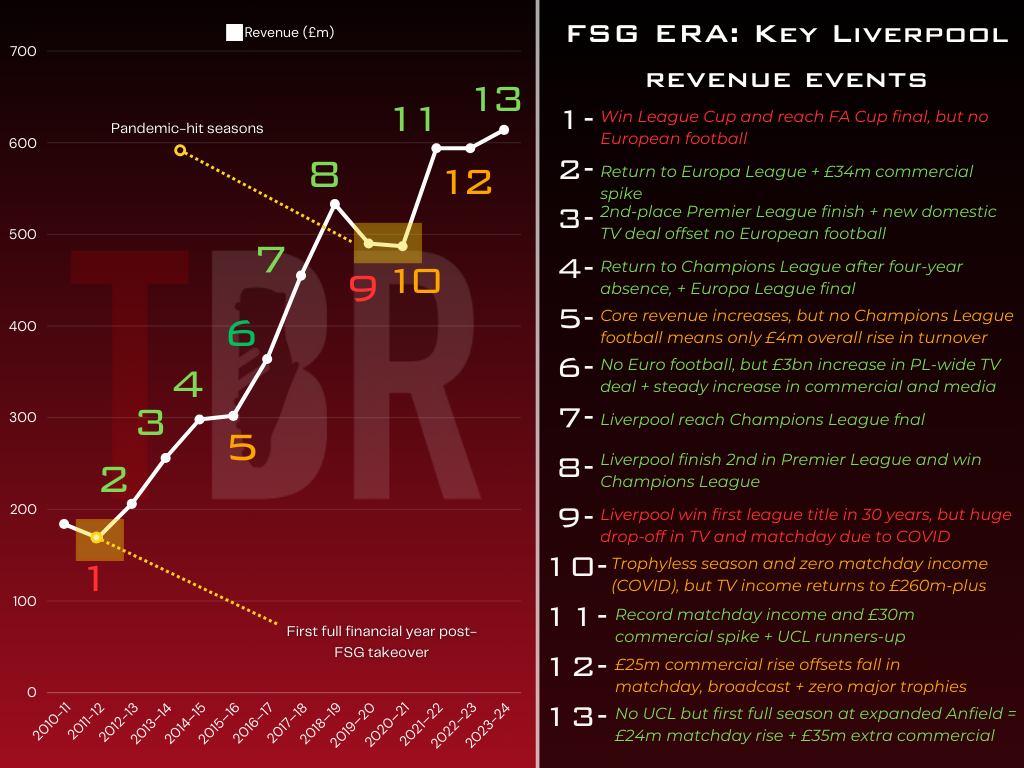

This is the masterplan at Anfield. FSG don’t take cash out of the club beside the occasional modest management fee, but they do plan to increase its value and eventually sell it for billions.

This is what’s known as capital appreciation. It relies on demonstrating the viability of the business model over time, meaning when Fenway feel they need to be ultra-disciplined in terms of cost control.

In the United States, the model is different.

Photo by Michael Regan/Getty Images

The franchise sports model – with no relegation, a ceiling in terms of costs, and a collaborative approach across leagues – makes baseball and ice hockey profitable in their own rights.

And the latest from the American finance sphere illustrates why FSG are all in on the franchise racket.

New benchmark for FSG as world-record Boston Celtics deal confirmed

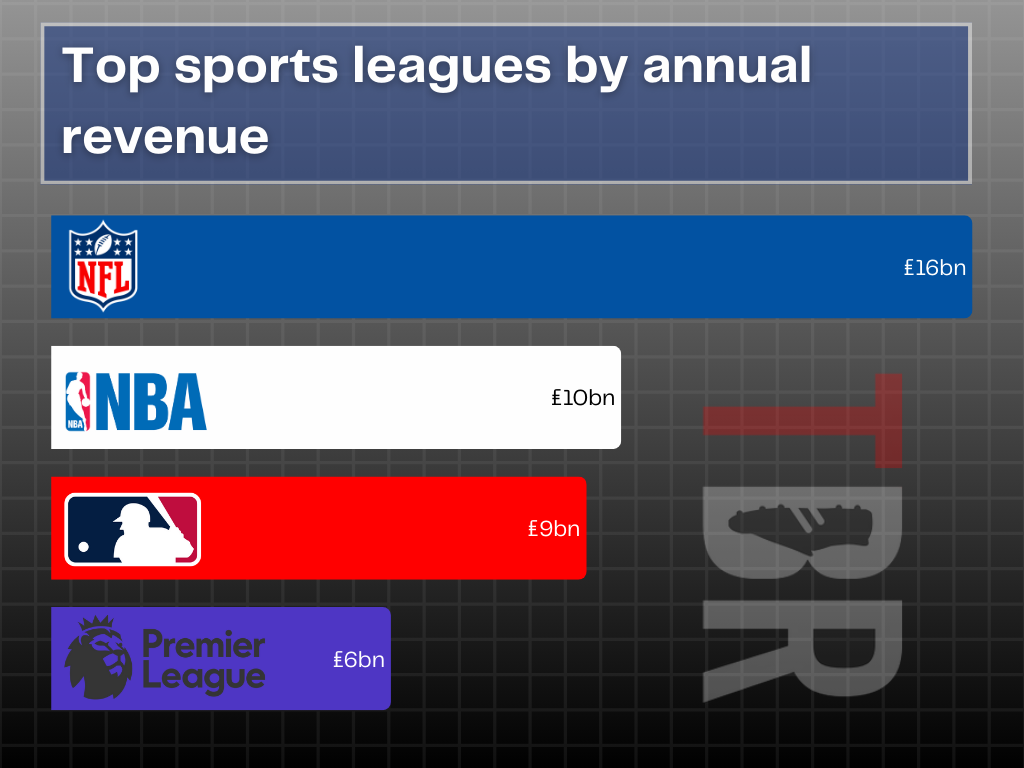

Sports in the United States generate more money than all the respective GDPs of all but the 70 richest counties on earth.

NFL is the most lucrative of the lot, followed by the NBA – those are the two areas that FSG aren’t yet directly involved in.

Credit: Adam Williams/TBR Football/GRV Media

A long-standing partnership with LeBron James, who was formerly a small stakeholder in the club itself before converting his shares into equity in FSG, has been seen as a means to one day changing that.

And when the Boston Celtics went up for sale in 2024, it seemed like the perfect fit. FSG’s offices are a stone’s throw away, after all.

The Boston Globe – a local outlet which, significantly, is owned by John Henry – reported last summer that the investment empire was indeed among the parties considering a bid.

However, FSG briefed earlier this year that they were not going to make an offer.

The process has now concluded, with a private equity-backed consortium beating off interest from new Everton owner Dan Friedkin to secure a £4.7bn deal, which is the biggest in sports history.

Liverpool’s rank in the world’s most valuable sports franchises

| Top-100 rank | Club | Value | 1-yr change | Revenue | Owner |

| 17 | Manchester United | $6.2B | +4% | $778M | Glazer family |

| 18 | Real Madrid | $6.06B | +16% | $844M | Club members |

| 35 | FC Barcelona | $5.28B | +7% | $836M | Club members |

| 40 | Liverpool | $5.11B | +8% | $713M | Fenway Sports Group |

| 46 | Bayern Munich | $4.8B | +8% | $781M | Club members |

| 51 | Manchester City | $4.75B | +7% | $855M | Mansour bin Zayed Al Nahyan |

| 61 | Paris Saint-Germain | $4.05B | +19% | $842M | Qatar Sports Investment |

| 65 | Arsenal | $3.91B | +9% | $558M | Stan Kroenke |

| 74 | Tottenham Hotspur | $3.49B | +9% | $660M | Joe Lewis family trust, Daniel Levy |

| 75 | Chelsea | $3.47B | ±0% | $615M | Todd Boehley, Clearlake Capital |

As far as FSG’s ambitions in basketball are concerned, something is still in the pipeline.

Las Vegas, which has long been mooted as the next expansion franchise destination, is being heralded as beachhead for FSG’s NBA masterplan.

For LeBron James, who has expressed his desire to move into the ownership side of the sport would be central to Fenway’s campaign, retirement is on the horizon.

That will likely be the catalyst for FSG to accelerate their interest in basketball.

Liverpool and ‘Premflix’: The next massive revenue stream?

If FSG were to pack up and sell tomorrow, Liverpool would probably fetch around £4bn. That is what the sale of a three per cent equity stake to Dynasty Equity for around £127m would suggest, anyway.

But the Boston owners are nowhere near exit value yet. For that to happen, the market would have to appraise the club at well beyond the £4.7bn paid for the Celtics.

How they get there is a matter of great debate in the football finance world.

Technology, most people agree, holds the key. Immersive reality, for example, can help better monetise overseas fans who don’t have access to Anfield.

A quantum leap in terms of media rights is another avenue. The Premier League’s domestic TV deal has soared for years but is showing signs of slowing down.

Internationally, the pie can continue to grow for a while yet, but this growth area will be all but exhausted at some point.

Credit: Adam Williams / GRV Media

How to increase the value of the rights, then? One idea is ‘Premflix’, the hypothetical name for a direct-to-consumer streaming service which would replace the various media partnerships.

Liverpool are interested in this model, but it’s along way off at present, despite the Premier League signalling it could one day move in this direction by taking its in overseas production in-house recently.

Last week, a new poll from YouGov suggests that two in five football fans would pay for an in-house streaming service.

Those aren’t the kind of numbers that would convince John Henry or many of his colleagues at Premier League shareholder meetings to take the plunge – not yet.

The sale of IP is cheap, easy and risk-free, so the league will be unlikely to make its own media product unless the value is massive and demonstrable.

{kind=link}