Taking over a Premier League football club offers instant celebrity and an equity stake in the most popular leisure pursuit in human history – but, as FSG have discovered, owning a club like Liverpool is also the most stressful investment a businessperson can ever make.

Unlike Liverpool, most businesses don’t have an army of emotionally invested fans attached who police the ownership of the organisation and eschew commercialisation over culture.

In the United States, where the vast majority of the Fenway Sports Group (FSG) empire is situated, there is less resistance to high prices, sport as entertainment and the closed-shop franchise league model.

In Major League Baseball and the National Hockey League meanwhile, John Henry and Tom Werner’s peers in boardrooms of other teams are seen as colleagues, not rivals. They are operating in each other’s mutual self-interest. If you increase the size of the pie, everybody eats better. That’s the philosophy.

In the Premier League, which is being ripped apart by in-fighting over the future of football finance, it’s an adversarial system. That’s something FSG want to change, as evidenced by Liverpool’s close collaboration with arch-rivals Manchester United on both Project Big Picture and the European Super League.

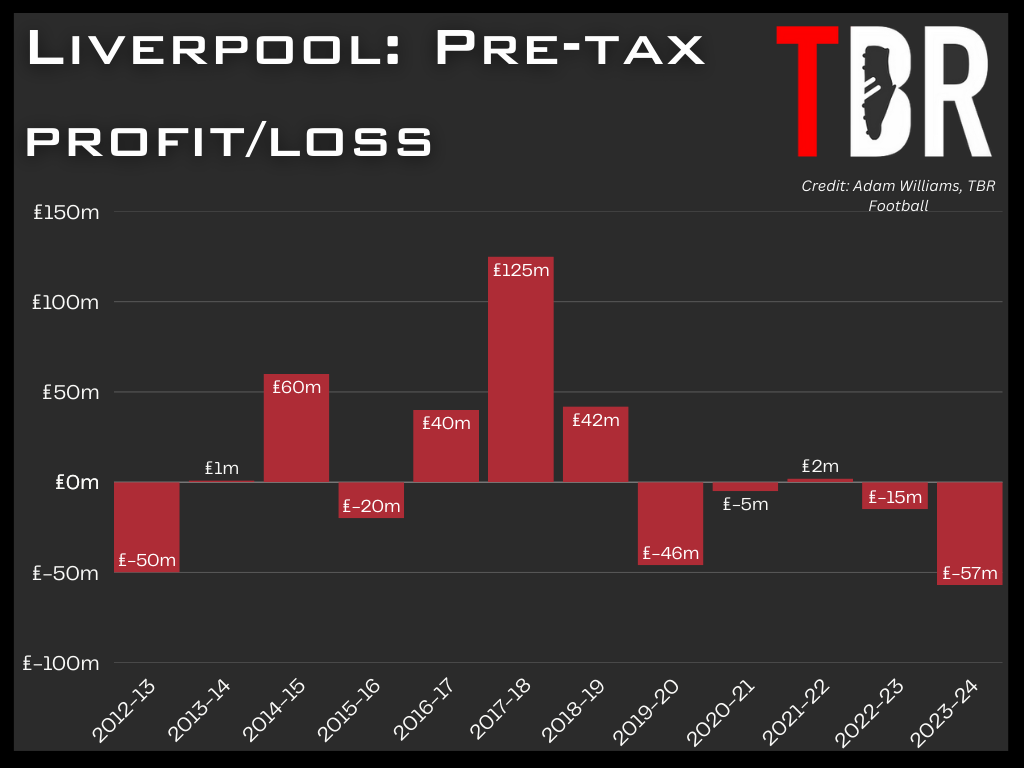

The competition and jeopardy inherent in the system means wages and transfer fees have spiralled, eaten into the bottom line. In turn, that is why, after spending upwards of £200m on the redevelopment of Anfield, FSG are well down on their investment on Merseyside.

Even as one of the best-run clubs in the world with one of football’s most famous brands that generates revenues of over £600m in a bad year, Liverpool are still a money pit for their owners.

Credit: Adam Williams/TBR Football/GRV Media

The Premier League title Arne Slot has won in his first season as Liverpool boss will lead to a nice bump in commercial income and prize money, but FSG still won’t take any cash out of the club.

So what is the long-term play? The Boston owners aren’t in this for altruistic purposes. One day, they will want a return on their investment that justifies the countless man-hours they have devoted to the project,

FSG’s capital appreciation model coming good as Liverpool valued at £3.9bn

It was somewhat telling that when, in the afterglow of the Premier League title celebrations, several senior Liverpool staffers reacted to a LinkedIn post that assessed the growth of the club’s value since 2010.

While it wasn’t a signal that a change of ownership is imminent, it was an indication that there is awareness within the club about FSG’s masterplan.

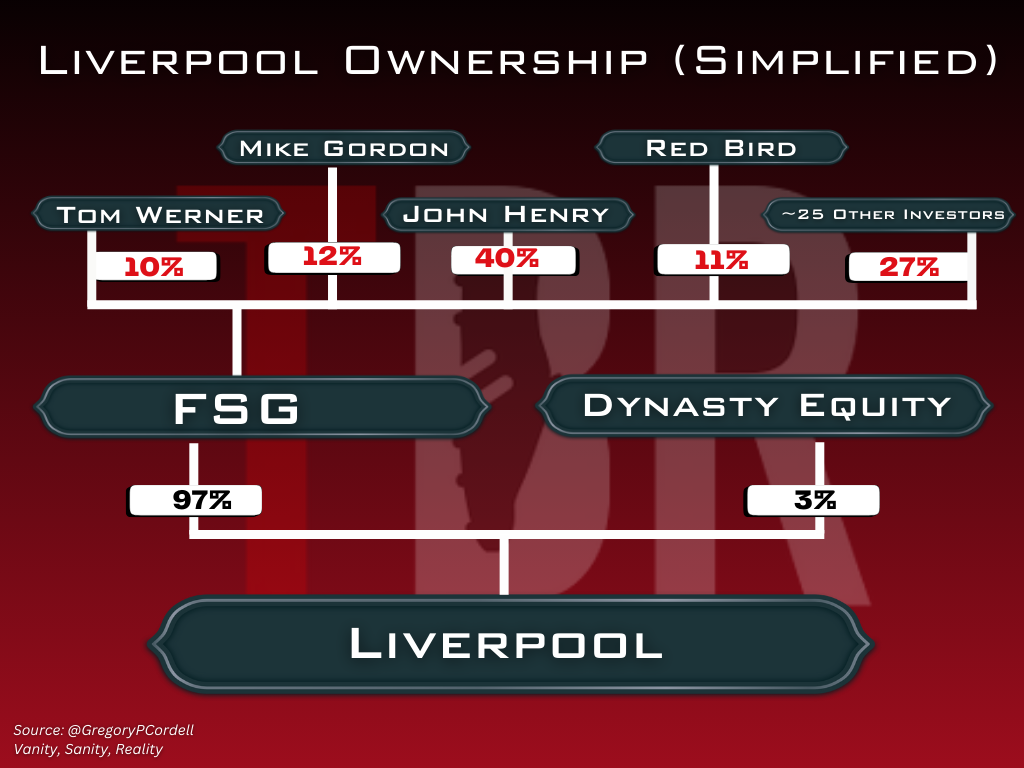

John Henry, Mike Gordon, Tom Werner, RedBird Capital and the dozens of other investors in the sports empire eventually want to flip Liverpool for a huge profit. It’s the capital appreciation model.

Credit: Adam Williams/TBR Football/GRV Media

In 2010, FSG paid around £300m to purchase the club from Tom Hicks and George Gillett. After clearing the club’s debt, the takeover valued Liverpool at around £400m.

Now, according to the latest appraisal from industry experts Sportico, Liverpool are worth £4.2bn, making them the fourth-most valuable asset in world football.

| Rank | Club | Value | Revenue (23-24) |

| 1 | Real Madrid | $6.53 billion | $1.13 billion |

| 2 | Manchester United | $6.09 billion | $834 million |

| 3 | FC Barcelona | $5.71 billion | $802 million |

| 4 | Liverpool | $5.59 billion | $773 million |

| 5 | Bayern Munich | $5.21 billion | $827 million |

| 6 | Manchester City | $5.16 billion | $901 million |

| 7 | Arsenal | $4.49 billion | $773 million |

| 8 | Paris Saint-Germain | $4.26 billion | $873 million |

| 9 | Tottenham Hotspur | $3.68 billion | $652 million |

| 10 | Chelsea | $3.57 billion | $590 million |

A profit of around £3.9bn in 15 years then would await FSG if they did decide to sell up.

- READ MORE: Rodrygo rules himself out of huge game in fear of injury after Liverpool begin talks to sign him

Liverpool takeover was ‘deal of the century’, says Kieran Maguire

If you had a spare few hundred million quid knocking about in 2010, Liverpool was a good place to invest.

As a compound annual growth rate, £300m to £4.2bn outperforms just about any stock or index.

It’s not hard to understand why, in exclusive conversation with TBR Football, University of Liverpool football finance lecturer Kieran Maguire described FSG’s takeover 15 years ago as the “deal of the century.”

And with FSG in the market for another club to take over, you wouldn’t bet against the owners in Boston repeating the trick, albeit at a smaller scale.

Liverpool are keen to set up a multi-club network and reappointed Michael Edwards to establish one.

Last summer, they pulled out of takeover talks for Bordeaux, who have since suffered administrative relegation to the lower tiers of French football.

CREDIT: Adam Williams / GRV Media

If the owners are still interested in the French market – which many multi-club prospectors are given its access to talent and recruitment benefits – then an opportunity could be about to present itself.

Several Ligue 1 club owners are expected to list their clubs for sale after the collapse of the league’s TV deal with DAZN.

{kind=link}