The Athletic has appointed Chris Weatherspoon as its first dedicated football finance writer. Chris is a chartered accountant who will be using his professional acumen as The BookKeeper to explore the money behind the game.

What follows is the latest in his series analysing the financial health of some of the Premier League’s biggest clubs. This time he’s tackled Newcastle United, but we’ve already published his analyses of Manchester United, Manchester City, Arsenal, Liverpool, Chelsea and Tottenham.

You can read more about Chris and pitch him your ideas. He has also written a glossary of football finance terms, here.

Newcastle United’s long wait for a trophy ended under Wembley’s arch just as evening was descending, the sun disappearing and, with it, 70 years of domestic strife. Mid-March’s victory over Liverpool in the Carabao Cup final marked the end of seven trophyless decades on Tyneside (the 1969 Inter-Cities Fairs Cup excluded) and, with it, perhaps, the beginning of something else.

Advertisement

As black-and-whites on the pitch and in the stands celebrated the end of an unwanted era, one emblem of their new era stood front and centre. Yasir Al-Rumayyan, club chairman, made his way onto the pitch and held up the trophy. He is also the governor of Saudi Arabia’s Public Investment Fund (PIF), Newcastle’s majority shareholder.

If Al-Rumayyan’s presence was unsurprising then it also did much to remind onlookers of how the club he now oversees arrived at this point. Since PIF took up a majority stake in Newcastle in October 2021 as the lead party in a consortium that wrested the club from the hands of Mike Ashley, the sovereign wealth fund’s financial commitment now stands at £528.7million ($703.4m) — £244.0m to buy the club (of the £305m total purchase price), and a further £284.7m injected into Newcastle since. In total, the club has received £335.4m in owner cash since the takeover.

Attributing their newfound success to money alone would be short-sighted — opponents Liverpool, after all, boasted a more expensive squad and one paid far more than Newcastle’s — but to say it has helped is an understatement. In just over three years, Newcastle have been transformed from a mid-table Premier League side into one regularly pushing for Champions League football. And now into cup winners.

In a financial sense, Newcastle’s post-Ashley world has been defined by what was a rare thing under their former owner: heavy losses. The first season under new guidance produced a pre-tax deficit of £72.9m, followed a year later with a £71.8m loss in 2022-23. Last season’s £11.1m in the red looks significantly improved against that backdrop, though were it not for a late-June flurry of transfer activity, the club would have posted three consecutive deficits in the region of £70m. Under Ashley, the club’s highest loss was £46.7m, incurred in the 2016-17 promotion season when Rafa Benitez was backed with significant sums (at least in the context of the Championship) to return Newcastle to the top tier.

Advertisement

What do Newcastle’s recent financials look like – and what’s their PSR position?

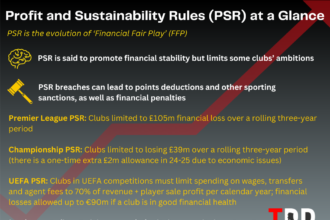

Newcastle’s combined pre-tax loss over the 2022-24 profit and sustainability (PSR) cycle totalled £155.8m, leaving them with just over £50m in deductible costs to find to come in under the £105m PSR loss limit. It looked a tight squeeze. Newcastle’s depreciation and non-player amortisation costs over the cycle totalled £10.9m, while expenditure on the women’s team — albeit rising under new owners — was just £3.6m in the same three-year period. Costs on the club’s academy and community development are unknown but ultimately came to at least the £36.3m the club needed to hit the £105m limit — though The Athletic estimates Newcastle’s PSR headroom last season was very much marginal.

As the end of June loomed, and with it Newcastle’s accounting deadline for 2023-24, sales were needed, with Alexander Isak and Anthony Gordon’s names raised in talks.

In the end, it was two other sales that did the trick. Elliot Anderson, an academy graduate, was sold for £35m to Nottingham Forest. Yankuba Minteh, who had spent the whole of his 12 months as a Newcatle player on loan at Feyenoord, went to Brighton for £30m. Between them, the sales generated £60m in profit, which proved enough to fill a previously gaping PSR black hole.

Those sales got Newcastle over the line from a Premier League PSR perspective, though UEFA’s tougher financial rules make the matter more complex. That Carabao Cup victory earned a return to European football, so Newcastle now have to ensure compliance with two sets of PSR.

As disclosed in the accounts, UEFA rules required the club to reduce player sale profits in 2023-24, to the tune of £30.4m. That pushed their pre-tax loss for UEFA’s purposes up to £38.1m.

The breakdown of the £30.4m reduction isn’t provided, but more than likely relates to the sale of Anderson and the $25m (£19.5m) departure of Allan Saint-Maximin to PIF-owned Saudi club Al Ahli.

UEFA rules look askance at the sort of deals Premier League clubs engaged in at large last June, whereby players swap clubs but the transactions are kept separate, ostensibly to book higher sale profits and boost bottom lines. Anderson’s move to Nottingham Forest seemingly meets these criteria; coming the other way was Forest’s reserve goalkeeper Odysseas Vlachodimos.

Advertisement

The exact figures involved have never been clear, but Newcastle’s accounts are instructive. UEFA requires sales proceeds on such deals to be measured at the value of the player in the selling club’s books, adjusted for any net cash paid as part of the deal. Anderson, an academy product, was held at close to nothing on Newcastle’s balance sheet, so under UEFA’s financial rules, the only profit that can be recorded from the deal is the difference between his sales price and the cost of Vlachodimos.

That has the balancing effect of requiring Newcastle to reduce the cost of acquiring Vlachodimos to zero, enabling us to see just how much they ‘spent’ on a goalkeeper they had little footballing need for. The answer is galling: Vlachodimos’ cost in the club’s books came to £22.8m. That puts him 12th on the list of Newcastle’s most expensive signings. He has played just 45 minutes of a Carabao Cup tie against AFC Wimbledon.

Signing the Greek goalkeeper was necessary in the short term, but the effects of the deal could be felt for years. Vlachodimos signed on a four-year deal, so Newcastle are now bearing £5.7m in annual amortisation costs for a player who is unlikely to contribute on the pitch. And that’s without including his wages.

Clubs who sell players to related parties cannot bank an accounting profit under UEFA rules. We project the profit on the Saint-Maximin deal was around £12m, so, returning to Anderson, that would mean Newcastle had to reduce their profit on his sale to Forest by £18m in their UEFA calculation. How that tallies with the £22.8m Vlachodimos ‘fee’ is unclear, but what’s certain is the value Newcastle derived from Anderson’s sale was well below what they’d have expected were they not a distressed seller.

In one sense, Newcastle were fortunate last season — UEFA’s football earnings rule, which limits club losses, wasn’t applied, as European football’s governing body gave clubs time to transition to new regulations. This season, club losses were limited to €80m over the previous two years but, without European football this year, Newcastle didn’t need to worry.

Why have losses increased so much?

In the 10 seasons between 2011 and Ashley’s eventual departure, the club’s funding from its owner was actually negative, to the tune of £29m.

Ashley might not have left fans with much they felt they could laud him for, but his tightfistedness did give the incoming owners more room to work with than might have been the case elsewhere. In all five seasons the club played in the Premier League between PSR’s introduction in 2013-14 and the last full campaign before the outbreak of the Covid-19 pandemic, Newcastle posted a profit.

Advertisement

That left the new owners with plenty of PSR headroom. The bulk of expenditure, unsurprisingly, went on the playing squad. Between Ashley’s final season and 2023-24, the club’s wage bill leapt £111.9m, while the cost of amortising player transfer fees was up a further £64.4m. Figures for the 2020-21 season were only over an 11-month accounting period, but even adjusting for that leaves a hefty increase over the past three years.

In terms of that wage bill, at £218.7m, it set a club record for the third year running, up 18 per cent on 2022-23. Yet while wages are growing, Newcastle have over-performed relative to their staff costs in both full seasons under Eddie Howe, first by a big margin — finishing fourth two seasons ago with the Premier League’s ninth-highest wage bill — and then closer to expectation — finishing seventh last season with the eighth-highest. Wage growth is unsurprising but Newcastle haven’t led the way either; Arsenal, Bournemouth and Aston Villa each displayed higher year-on-year growth last season.

A combined look at Newcastle’s wages and player amortisation costs as a proportion of revenue is instructive for explaining growing losses. In 2018-19, before Covid-19 hit, 77 per cent of the club’s income went on such costs, the fifth-lowest ratio in the top flight. Last season, that figure had jumped to 98 per cent. In other words, nearly all of Newcastle’s revenue (excluding player sales) was consumed by wages or amortisation.

That’s a clear shift in strategy, though it’s notable that eight other clubs still spent proportionally more. Newcastle have upped their player spending significantly in recent years, but it’s not the only thing to have increased losses. Non-staff expenses excluding depreciation have rocketed, up £44.5m (191 per cent) since before the pandemic. That’s a product of multiple factors, including the higher cost of hosting Champions League football last season, a high-inflation environment and generally being looser with the pursestrings.

Even with club record revenues of £320.3m last season, increased income has been outstripped by rising costs. That has left operating losses hovering around the £68m mark in each of the past two seasons and while six Premier League clubs posted a worse day-to-day result than Newcastle last season, a key reason they ran so close to the PSR brink was their pretty awful record of selling players for profit.

Where other clubs have routinely turned to player sales as a way to boost bottom lines, Newcastle have long been poor sellers. Between 2020-21 and 2022-23, they made just £10.4m profit on outgoing players. Thirty-three English clubs made a greater profit during those three seasons.

The sales of Anderson, Minteh and Saint-Maximin generated a club record £69.8m in player sale profits in 2023-24. As we’ve seen, that figure was inflated by the Anderson-Vlachodimos deal.

This season, Newcastle sold Miguel Almiron for £11m, a deal they will recognise a profit of about £9m on. A new Adidas deal (more on that in the next section) and a rise in gate receipts will boost revenue, but banking extra merit payments for finishing high up the table has become more important, as Newcastle could do with offsetting the £30m in lost UEFA income this term. With operating losses running high and no other sales of note, it looks unlikely the club has a lot of room for manoeuvre before the end of June, though 2025-26 will see another £70m-plus loss drop off their PSR calculations.

Advertisement

Commercial focus

One big gripe fans held under the Ashley era was the sluggish growth in commercial revenue. In his last season, Newcastle’s commercial income was £17.6m, only the 14th highest in the Premier League. That did come in an 11-month accounting period but even employing fairly generous logic and pro-rating the sum to 12 months doesn’t move the club up.

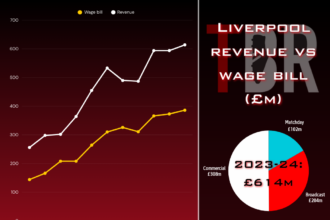

Fast forward three seasons and commercial revenues have more than tripled to £83.6m. From lower mid-table, Newcastle’s income here is now the largest outside the traditional ‘Big Six’. Their 375 per cent commercial income growth in the past three seasons is the highest of any club to have spent both of the two compared years in the top tier. No one else comes close — the next-highest growth from a club who was in the Premier League in both 2020-21 and last season is Fulham’s 155 per cent.

Newcastle’s commercial income has been of wider concern ever since PIF walked through the door, with rival clubs heeding past lessons of state-linked sponsorships at Manchester City and Paris Saint-Germain. It was broadly for that reason clubs passed new associated party transactions (APT) regulations in December 2021, seeking to limit any opportunity for club owners to inflate revenues through generous sponsorship deals with linked companies.

Those same rules were recently deemed “void and unenforceable” after a legal challenge by Manchester City. A second such challenge is now ongoing.

In any case, the new APT rules meant all deals Newcastle made with PIF-linked companies were subject to a fair market value assessment by the Premier League.

The club’s accounts detail the quantum of commercial income derived from related parties, though there’s an important distinction here between related parties and associated ones. Noon, the club’s sleeve sponsor, and Sela, the club’s front-of-shirt sponsor, are each PIF-owned, and constitute related parties. Saudia, the club’s official airline partner, isn’t PIF-owned, but likely fits the definition of an associated party. To that end, the reported £3m Newcastle earn annually likely isn’t included in the related party commercial income disclosed in the accounts. Confusing enough?

Newcastle’s accounts detailed that the club earned £29.0m from PIF-owned related parties last season. The Noon deal generated £6.7m for the club in 2022-23 so, assuming that remained consistent, the Sela agreement works out at £22.3m annually — a little below the widely reported £25m figure.

Related party income accounted for 35 per cent of Newcastle’s commercial income last season, up from 15 per cent a year earlier. Assuming the £3m from Saudia isn’t included in the related party income, bundling that in bumps the figure up to 38 per cent.

There have been other PIF link-ups to go alongside those three sponsorship deals. Savvy Games Group, a PIF-owned entity, came on board as the club’s ‘official summer tour partner’ during last year’s pre-season trip to Japan. A week later, the second iteration of the Sela Cup, a pre-season tournament, was held at St James’ Park. Somewhat separate to commercial income, Sela’s brand adorned 32,000 free scarves handed out to supporters in the Newcastle end at Wembley last month; similar generosity had been afforded to the 6,000 fans who travelled to local rivals Sunderland for an FA Cup tie in January 2024.

Advertisement

Meanwhile, PIF even took to advertising itself on St James’ Park hoardings this year. Using the club’s home as a marketing space for the owner’s other companies was one of Ashley’s most despised transgressions, though the difference now is that PIF is providing far more funding than any matchday advertising could ever hope to offset. It is not known what PIF paid for the spaces.

While little attempt has been made to hide newfound links to PIF and Saudi-backed companies, they form part of a wider commercial strategy undertaken since late 2021. Critiques of the non-existent attempts to grow commercial income under Ashley were well-founded; by the time he sold up, Newcastle’s commercial revenues were actually less than in his opening year in charge.

The growth in related party income of £29.0m in the past two seasons only slightly eclipses growth seen elsewhere in the club’s commercial portfolio (£28.0m), though again we do have the Saudia caveat.

Since the takeover, Newcastle have inked numerous new deals, significantly broadening their commercial activity. The 2023-24 season saw agreements signed with InPost, BetMGM, Fenwick, Quidd, Sportsbet.io and Straightline NE Limited. Fun88, moved aside after six years as the club’s front-of-shirt sponsor, nevertheless retained links on Tyneside by becoming the club’s Asian betting partner.

Activity has continued this season. Commercial deals have been made with Red Bull, JD, VT Markets and Destra. Most important has been a shift to Adidas as the club’s kit supplier. The deal’s annual worth to Newcastle is between £25m and £40m, dependent on various factors, but even at the low end of the range, this single agreement would be almost equal to the club’s entire annual commercial revenues across much of Ashley’s reign.

Newcastle have a long way to go to catch up to the ‘Big Six’ in England — Arsenal were bottom of that pack last season yet still booked commercial income of £218.3m — but they’ve rapidly moved into position as the highest-earning of the rest. With Adidas now in tow, commercial revenues are likely to tip over the £100m this season.

How much has been invested – both on and off the field?

While there has often been talk of a club constrained, Newcastle have still managed to invest heavily in their squad. It was such spending that edged them perilously close to a PSR breach. At the end of last season, their existing squad had cost £605.1m to assemble, up from £233.3m just three years earlier. It meant Newcastle were, again, top of the pile beyond the ‘Big Six’. Moreover, the club’s squad was actually the 10th-most expensive in world football at the end of last June.

Last season, Newcastle spent £206.1m on new players, joining a group of nine other English clubs to have splurged more than £200m in a single season. Without the £22.8m Vlachodimos fee, the figure would have been lower — but still a club record.

Across the last three seasons, Newcastle have spent a total of £508.6m on signing players, the sixth most in England in that time. On a net basis, their £407.7m spend ranks them fifth.

Advertisement

That is a departure from the past but it is not as outlandish as many may have expected back in October 2021. Chelsea’s largesse has dwarfed everyone else, but Newcastle aren’t sitting one spot behind them either. There has been significant investment in the club’s squad, but they continue to play catch-up with domestic big spenders. Even so, with PSR biting, spending in 2024-25 has slowed dramatically; the club’s net spend this season is just £20m.

Away from the playing squad, there’s been a noticeable uptick in capital expenditure. Spending on infrastructure under Ashley was damningly low, not even getting above the £1m mark in his final six years at the helm.

Since his departure, over £40m has been invested in fixed assets, principally in the form of improvements at St James’ Park and the club’s training ground, alongside repurchasing land behind the Gallowgate End (sold by Ashley) and, since then, investing in the Stack leisure hub and fanzone that now sits there.

Yet while capital spending is to be welcomed, one key issue remains very much up in the air. Despite months of discussion, Newcastle are still to decide what to do about their home stadium: improve or move.

A decision on the fate of St James’ Park was previously signalled for the first quarter of 2025, a deadline now almost certain to be missed. Some senior figures prefer to leave the club’s longtime home and oversee a new build on nearby Leazes Park but, in lieu of a firm decision being made, plans for the renovation and expansion of the current stadium continue to be looked at.

As The Athletic reported in January, talks have not commenced between the club and key stakeholders, and no decision has been made on the final design of a stadium, new or old, nor its size. Planning permission has not been applied for. When a decision will be arrived at is anyone’s guess, but improving matchday revenues seems necessary if Newcastle are to compete with the elite. Four English clubs currently boast over £100m in annual gate receipts; Newcastle, even with recent substantial growth, are only at half that.

Overall, via PIF and its consortium partners Jamie Reuben and Amanda Staveley (since departed), Newcastle received £285.4m in new cash from their owners in the three years to the end of last season, all of it as equity (ie, no loans). Only Chelsea, Fulham and Everton received more, with Fulham and Everton’s funding primarily going towards infrastructure. Chelsea are another matter entirely. Since the end of last June, Newcastle have received a further £50m from their owners.

One curiosity of Newcastle’s funding since the takeover is the existence of a £50m term loan facility, taken out with HSBC in 2022-23, presumably to help with short-term cash flow needs. That’s not a worry — it’s quicker to get money from there than call in capital from Saudi Arabia — but the loan’s existence has hit the bottom line, with £9.5m in interest costs adding to Newcastle’s losses over the last two seasons. Without those costs, the club would have had more PSR breathing room.

Advertisement

What’s next?

The greatest unknown in Newcastle United’s future is PIF’s continued interest and financial commitment. While PSR has limited the scope to which the sovereign wealth fund can pour in money unfettered, losses have still been hefty. Very much still in a growth stage, Newcastle are some way from standing on their own two feet.

Untangling PIF’s largely opaque finances is close to impossible, but even the snippets we can see suggest the fund’s investment in Newcastle is at the lower end of its broad scale. Details of PIF’s financial commitment in its aggressive move into golf, via the LIV Golf brand, serve as a decent point of comparison.

Across its first 18 months in operation to the end of 2023, Liv Golf Ltd, under which the upstart tour’s activities outside the United States sit, had accumulated pre-tax losses of £639.7m, on total revenues of just £42.0m. PIF provided £609.7m in funding during that time, a figure that has only grown since.

The losses visible in the UK-registered company literally aren’t the half of it. Per filings for LIV Golf Investments Ltd, a Jersey-based holding company, the authorised share capital of the holding company now sits at $4.24bn, or £3.4bn per our estimation. If the UK company accounts for £610m of that, that leaves £2.79bn attributable to LIV Golf Inc., based in the U.S., the vast majority of which is covering losses. That overall £3.402bn includes a January 2025 capital contribution of £270m — or less than £15m shy of the total cash PIF has pumped into Newcastle.

That can be read two ways. PIF’s financial investment in LIV Golf has been an order of magnitude higher than on Tyneside; is its golf tour a bigger priority? Alternatively, the spending on LIV could point to them barely scratching the surface to date at Newcastle; if it is willing to pump over $4bn into golf in just a couple of years, who knows how deep its pockets might be for a Premier League football club?

Whatever the truth of the matter, Newcastle’s immediate future is reliant on PIF’s attitude and funding. A key reason the stadium plans remain mired in stasis is that all the big decisions, and particularly the expensive ones, must go through the Saudi branch of Newcastle’s ownership group. Without its say-so, nothing big gets done.

How much wider factors will influence PIF plans on Tyneside is unknown. Seeking to stem the tide of falling oil prices, PIF has reportedly scaled back or cut various projects. Giga-projects, including the futuristic city of Neom, have been reduced already; it’s unclear if such cuts would reach St James’ Park.

Advertisement

From a PSR perspective, Newcastle are unlikely to be as pinched as a year ago but their headroom still looks limited, at least until the end of June. Once the 2025-26 accounting period rolls around, and the big loss of 2022-23 is gone from their calculation, they’ll have greater scope to spend domestically.

On the European stage, things will remain tighter. Clubs are allowed lower losses and UEFA is more stringent than the Premier League. Separately, UEFA’s squad cost ratio rule limits what clubs can spend on wages and amortisation; Newcastle, as we’ve seen, have hardly skimped there recently. Their headroom for next season’s limit — where clubs can spend only 70 per cent of relevant turnover on squad costs — looks tight, especially without player sales to boost that relevant turnover figure. The squad cost rule is assessed over calendar years rather than accounting periods; if Newcastle make a big sale this summer, it could be with that rule firmly in mind.

Of immediate focus is a return to the Champions League. Achieving that would bring not just sporting glee but could also solve many of their financial problems, with the tournament’s new format providing clubs with even more wealth. Newcastle’s earning potential would be hampered by UEFA rewarding clubs for historical performance, as it was in 2022-23, but there would still be plenty of cash to go around. The chance to further increase commercial income wouldn’t be sniffed at either.

Newcastle United are unrecognisable from October 2021. Being backed by one of the richest sovereign wealth funds on the planet has made a mark, believe it or not. Football’s financial regulations may have slowed that impact, but the club have still spent heavily.

The pump has been primed. Success has started to flow. How quickly more follows is anyone’s guess, but finishing in the top five next month should allow Newcastle’s owners to loosen the taps once more.

(Photos: Getty Images; design: Eamonn Dalton)

{kind=link}